Items Needed To Apply for a Home Loan

Applying for a home loan these days is not for the “weak at heart”! It is a pain-in-the-neck process no matter how much money you have or which lender you choose. So mentally prepare yourself for a hassle, and you won’t be disappointed. ;-D

Applying for a home loan these days is not for the “weak at heart”! It is a pain-in-the-neck process no matter how much money you have or which lender you choose. So mentally prepare yourself for a hassle, and you won’t be disappointed. ;-D

NOTE: Read The Perfect Loan File on Forbes for details.

There is a lot of paperwork required in order to obtain a home loan. Plus, you will have to provide much of the paperwork multiple times throughout the loan process because of new lending standards (Dodd-Frank Wall Street Reform and Consumer Protection Act legislation and the Patriot Act).

Lenders are now required to verify certain items several times through the process…so please don’t get offended or frustrated when they ask you for something that you have already provided them.

Here’s what you will probably need to apply for a home loan (aka, mortgage):

- Proof of identity for borrowers including driver’s license and Social Security number.

- Address history for three years.

- Copy of tax returns for past 2 years.

- Banks names and numbers for all checking and savings accounts.

- Bank statements for the past 3 months.

- Documentation of all income including pay stubs for past 2 months.

- Proof of bonuses for 2 years if applicable.

- W-2 forms showing income for past 2 years.

- Job history for past 2 years.

- Net worth sheet with list of all assets and liabilities including account numbers.

- Most recent 401K statements and other retirement accounts.

- Copy of gift letter if applicable.

- If self-employed, copy of balance sheet.

- Divorce decrees if divorced in the past 2 years.

- Proof of residency, if applicable.

- College transcript if you were a student in the past 2 years.

- Bankruptcy discharge papers, if applicable.

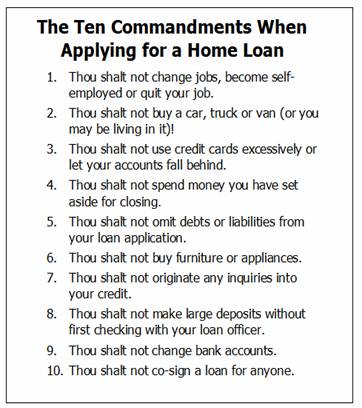

What Not To Do

Maybe you’ve just gotten married. Maybe you got a raise … or maybe you’re just plain sick of renting. Whatever the case, you’ve decided that it’s time to buy a house. You’ll be given all kinds of advice and pointers about what you should do and how you should do it, but there are things you shouldn’t do that are equally important.

Don’t be deceptive or dishonest when you’re filling out your loan application. Even if you get away with fudging the numbers a little to secure a higher loan (which is loan fraud), what’s the payoff you’re looking for? A monthly payment that you can’t truly afford?

Avoid moving your money around. To eliminate potential fraud and provide a degree of quality control, a lender will review the source of funds for your down payment and closing costs. Most likely, you will be asked to provide recent statements for any of your liquid assets. This includes checking accounts, savings accounts, money market funds, certificates of deposit, stocks, mutual funds, and even your 401K and retirement accounts. If you have been moving money between accounts during that time, there may be large deposits and withdrawals in some of them, which could make it more difficult for the lender to document properly.

Once you’ve been approved for a certain amount, resist the temptation to make any big purchases that could affect your ability to service the loan. Examples might be a new car, a boat, or expensive furnishings.

Sure you may be able to afford the mortgage and a car payment, but what if an unexpected expense comes along that causes your monthly budget to become unbalanced—you’ve got a shiny new car, but you may have trouble affording that and gasoline, and the mortgage, and the utilities. You’re caught in a situation where you’ve over-extended yourself. Even if you’re able to make it work on a month-to-month basis, you may have trouble putting money to your savings account.

Sometimes, knowing what not to do is just as important as knowing what to do.

Big Bank vs. Local Lender

A “big bank” is Chase, Bank of America, Wells Fargo, etc. They may be great banks but, that doesn’t necessarily mean they are great mortgage lenders.

Check your loan officer at https://www.nmlsconsumeraccess.org.

To be fair, I have seen a handful of deals, with big bank lenders, that went very well. However, several of them were for employees of the bank…who had the inside advantage.

Lenders to Consider

Lenders (loan officers) that my clients have used in the past:

Will Swallen

Bay Equity

713.558.0364

www.LoanWithWill.com

David Krichmar

DaveYourMortgageGuy.com

832-689-6012

Deesh Nair

Motto Mortgage

Deesh.Nair@mottomortgage.com

914-844-7797

REALTORS DON’T “JUST” SELL HOUSESReal estate agents don’t “just” sell houses; we sell a SERVICE to guide home buyers and sellers through the entire real estate transaction, which usually takes several months. We are more like real estate consultants than we are salespeople. That’s probably why 86 percent of all home buyers and sellers choose to hire a real estate agent when buying or selling a home! Buying or selling a home is not like buying or selling a TV, a computer, or a car. You can’t buy/sell a home in one day…even if the buyer is paying cash. There are MANY legal aspects, deadlines, and requirements that most people are not trained to handle. What’s more…mistakes along the way can cost you thousands and even hundreds of thousands of dollars. The financial risk is much greater than just about anything else you may buy.

Please read the list of my value-added services for home buyers |

FREE GUIDES & REPORTS

Click Image Below to Download a Guide or Report

![]()

View Helpful Videos on My YouTube Channel

Why You Should Hire Me

Candid Advice—I promise to give you candid advice on all homes and areas so you can make the best decisions. I won’t ignore potential defects that can cost you money, or effect your resale value, in the future…I point them out to you! My job is to protect you from defective homes as much as possible while helping you make a sound financial investment. (Read client testimonials)

Candid Advice—I promise to give you candid advice on all homes and areas so you can make the best decisions. I won’t ignore potential defects that can cost you money, or effect your resale value, in the future…I point them out to you! My job is to protect you from defective homes as much as possible while helping you make a sound financial investment. (Read client testimonials)

Local Area Expertise—This isn’t just my business…it’s where I work and live (for 20 years) so I really know the area. I will help you narrow your options and find the best neighborhood for you based on your specifications. For long-term resale value, the neighborhood you choose is just as important as the home you buy. (Download my Ultimate Sugar Land Guide)

Great Pricing Data—I will give you the most in-depth data you have ever seen…to help you make the wisest decisions. This includes a professional CMA when you are ready to purchase a specific home…so you don’t pay too much. (Also see Pricing a Home Correctly)

Premium Customized Home Searches—Yes, you can search on your own, but no other home search available can filter down to the school level…and filter out the subdivisions that may be known to flood. Tell me exactly what you want, and I can narrow down your options better than any search you have access to. (Request a Premium Customized Home Search)

Video Walkthroughs—If you or your spouse lives out of the state or country, then you will enjoy my detailed video walkthroughs. I have sold multiple homes to out-of-area clients “sight unseen” by providing High Definition video walkthroughs of potential homes. My videos show front and back yards, closets, pantries, laundry rooms, and the garage…as well as the entire home. This gives you a complete picture of the house (unlike those silly Matterports). I also point out any potential defects or deferred maintenance that I see. (view sample video walkthrough)

Easier Process—Moving your family (and possibly changing jobs) is stressful enough. I’m your transaction manager and will guide you, step-by-step, through the process so you never miss an important deadline. I assist with inspections, repair negotiations, home warranties, HOA compliance inspections, hazard insurance, surveys, appraisals, title commitment, home warranties, title company, and more. (Get Details of My Value-Added Services)

Connect With Sheila